Mercury

Banking and financial workflows built for startups

Gallery

About Mercury

Mercury is the bank startups actually want. It's not technically a bank, it's a banking platform built on top of partner banks, but the experience is what early-stage founders pick first. Wires send fast, the UI doesn't insult you, and the integrations work.

For Y Combinator companies and most venture-backed startups, Mercury is the default opening account. The product respects that founders are busy and that finance ops should be a tool, not a job.

What Mercury offers

Mercury has three product layers. Mercury Banking is the checking and savings account, plus debit cards and wires. Mercury Treasury is automated yield on your idle cash, currently around 5 percent through money market funds. Mercury Venture Debt extends growth capital to qualified startups.

The banking core covers ACH, wires, checks, and international payments. The Treasury product runs your cash above a threshold into yield-bearing instruments automatically. The IO product lets you spin up subaccounts, virtual cards, and approval workflows for accounts payable.

The IO bill pay layer

Mercury IO is the newer accounts payable feature. You upload bills, set approvers, and Mercury pays them by check, ACH, or wire. It competes with BILL and Ramp for SMB AP. The product is younger but well-integrated with the bank account, which simplifies reconciliation.

Who Mercury is for

Mercury fits venture-backed startups, indie SaaS companies, agencies, and bootstrapped tech businesses. The shared thread is comfort with online-first banking and an expectation that the bank treats you well as a customer.

Mercury isn't built for cash-heavy businesses. There's no easy way to deposit cash. If your business is a restaurant or a retail store, you'll need a traditional bank with branches. Most software businesses never need that.

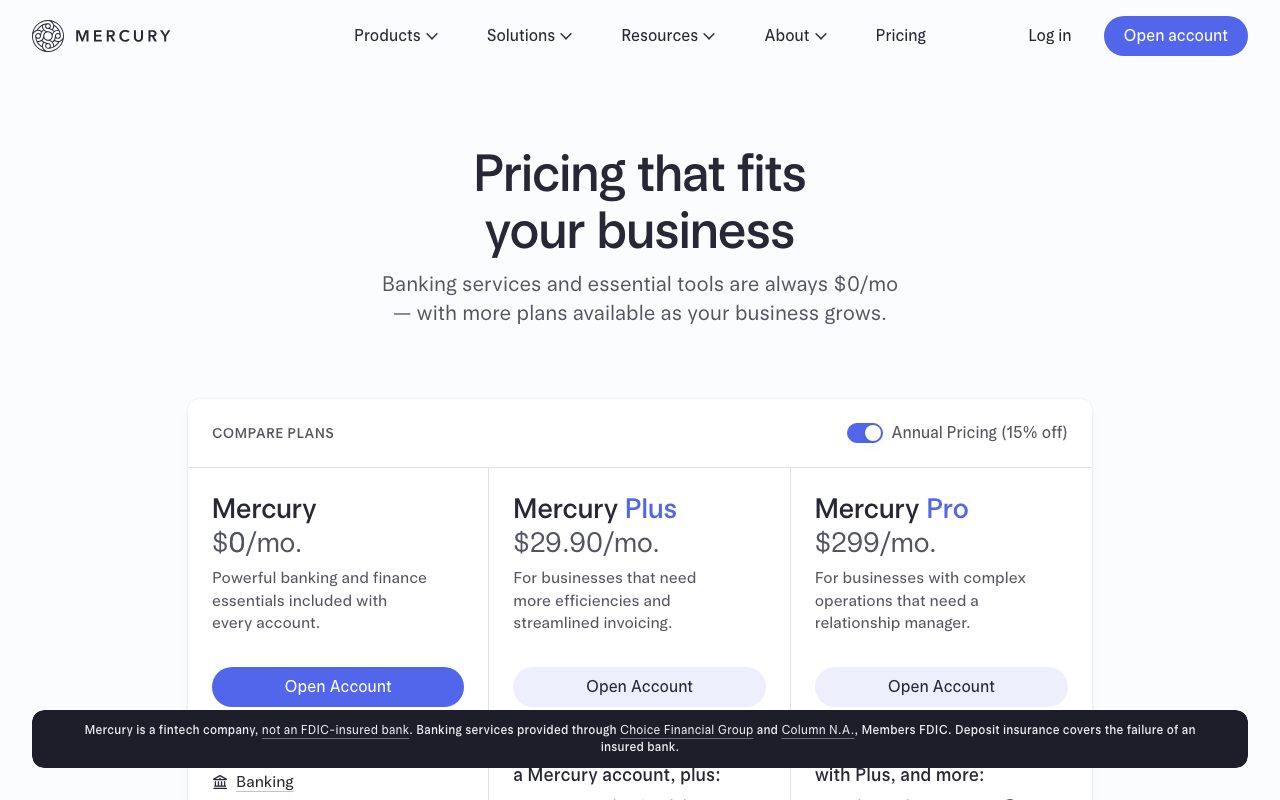

Mercury pricing

Mercury Banking is free for most businesses. There's no monthly fee, no minimum balance, and ACH is free in both directions. International wires have small fees, and you get five free domestic wires a month with a large balance.

Mercury Treasury has a small management fee that gets eaten by the yield. Mercury IO has tiered pricing for AP volume. The platform monetizes through interchange on debit cards and the spread on Treasury, similar to most modern challenger banks.

Mercury features that matter

The dashboard is genuinely well-designed. Transactions are searchable, taggable, and exportable. Wires send within minutes during business hours, faster than most traditional banks. Virtual debit cards spawn instantly with custom limits.

The API is real and supported. Engineering teams can pipe transaction data into accounting tools, anomaly detection, or internal dashboards. Plaid is integrated for connecting other accounts. The integrations include QuickBooks, Xero, NetSuite, Zapier, and many tax tools.

Founder-focused touches

Mercury has features specific to startup workflows. SAFE and convertible note tracking, cap table integration with Carta, founder identity verification that doesn't require an in-person visit, and account opening in days rather than weeks. These small things matter.

Tradeoffs

Mercury is not FDIC-insured directly. The deposits are placed at partner banks that are FDIC-insured. The legal structure is sound, but it's worth understanding. In a banking crisis like SVB in early 2023, Mercury moved fast to protect customers, but the experience reminded everyone that fintech and banking are different.

Mercury also has more conservative account closure policies than traditional banks. If your business pattern looks unusual, the compliance team may flag it, sometimes without warning. This has happened publicly to some founders. Most companies never see it, but it's a real risk to know about.

Mercury is the default startup bank for a reason: speed, polish, and Treasury yield. Pair it with a backup account at another bank for resilience.

Mercury vs alternatives

Compared to Brex, Mercury is more banking-shaped while Brex is more spend-and-card-shaped. Brex doesn't offer wires the same way. Compared to Ramp, Ramp is purely cards and bill pay, not a bank account. Most startups end up with one of each.

Compared to traditional banks like Silicon Valley Bank or Chase Business, Mercury is dramatically faster and more developer-friendly, with weaker physical presence and crisis history that's still recent. See our best startup banking guide and SVB alternatives roundup.

Bottom line on Mercury

Mercury is the right primary bank for most software-shaped businesses. The product is fast, the UI is clean, and the Treasury yield is meaningful on any balance over six figures. The IO layer increasingly removes the need for a separate bill-pay tool.

The reasonable strategy in 2026 is Mercury as primary, a second account at a traditional bank like Chase as a backup for crisis scenarios, and Brex or Ramp on top for cards and expenses. That stack handles 95 percent of startup finance ops without thinking about it.

Mercury for early-stage startups

The pattern for most early-stage startups using Mercury starts simple. One operating account for incoming and outgoing transactions. One Treasury account for runway above three months of burn earning yield. A handful of debit cards for founders and early employees. That setup covers daily operations cleanly.

As the company scales past 10 to 20 employees, Mercury IO becomes valuable for vendor bill pay. Subaccounts let you segregate funds for taxes, payroll, or specific projects. The expense management gets formal: virtual cards per category, budget limits per team, automated receipt capture. Mercury supports all of this without forcing an upgrade to a different tool.

SVB collapse and what changed

The Silicon Valley Bank collapse in March 2023 reshaped how startup founders think about banking. Mercury was a major beneficiary as founders fled SVB. The crisis also exposed real questions about fintech versus traditional banks. Mercury responded by adding the Mercury Vault product, which sweeps deposits across multiple FDIC-insured banks for higher coverage limits.

The lesson many founders took away: keep operating funds at one provider but maintain a backup account elsewhere. Mercury plus a small Chase Business or local credit union account is the resilient setup. The cost is minimal; the protection against another crisis-level event is real.

Mercury Treasury yield mechanics

Mercury Treasury invests idle balances into money market funds and short-term Treasuries through partnered brokerages. The yield tracks Federal Reserve rates closely. As of early 2026, the yield is around 5 percent annualized, which makes a meaningful difference for any startup with six or seven figures in the bank.

The funds aren't FDIC-insured because they're investments rather than deposits. The underlying instruments are very low risk (US Treasuries, money market funds), but they're not the same as bank deposits in regulatory terms. Most CFOs think this risk-return tradeoff is straightforward. A handful of more conservative finance teams stick to FDIC-insured accounts only.

Common Mercury questions

Can Mercury replace a CFO's bank? For most startups under $50M ARR, yes. Above that, larger companies often add a relationship at a major bank for capital markets activity, debt facilities, and complex treasury operations. Mercury can serve as primary even at scale, but enterprise-grade banking services require more breadth than Mercury currently offers.

How does Mercury compare to Brex? Different categories. Mercury is a bank account first, with cards and bill pay added on. Brex is a card and spend management product. Many startups use both: Mercury for the account and wires, Brex or Ramp for cards and expenses. The overlap on bill pay is increasing.

Does Mercury work for non-US founders? Mercury is generally for US-incorporated entities. International founders typically need to set up a US Delaware C-corp first, which most venture-backed startups do anyway. Wise Business or local options serve founders staying outside the US incorporation path.

Mercury IO bill pay analysis

Mercury IO has matured fast. The product handles invoice ingestion via email forwarding, OCR-based data extraction, configurable approval workflows, and scheduled payments. The integration with the bank account means reconciliation is automatic. For most SMBs, IO eliminates the need for a separate AP tool.

The remaining cases where dedicated AP tools like BILL still win are complex multi-entity setups, deep accountant integration, and specialized AP workflows like check approval routing across multiple departments. Most simple businesses can run their AP entirely within Mercury IO and skip the additional tool. That bundling continues to compress what used to be a separate product category.

Final take on Mercury

Mercury has earned its place as the default startup bank by getting the basics right. Fast wires, clean UI, real API, and a Treasury product that makes idle cash productive. The team treats founders like customers worth retaining. After the SVB crisis, Mercury responded faster and more transparently than most banks would have, which built trust during a critical period.

The competitive environment has tightened. Brex, Ramp, Rho, Arc, and Meow all serve adjacent or overlapping needs. The differentiation between modern fintech offerings has narrowed. Mercury's edge is being the most banking-shaped product in the segment, with cards and bill pay as supporting features rather than the main event.

For most software-shaped startups in 2026, Mercury remains the right primary banking choice. Pair it with a backup at a traditional bank for crisis resilience. Add Brex or Ramp for cards if you want stronger spend management. The combined stack handles modern startup finance ops well at reasonable cost. Mercury continues to ship features and improve the product steadily, which is what you want from a long-term banking partner.

Tutorial / Demo

Key Features

- Business checking and savings accounts

- Debit and corporate cards

- Treasury yields on idle cash

- Bill pay and ACH/wire transfers

- API access for programmatic transfers

- Integrations with QuickBooks and Xero

Pros & Cons

What we like

- Modern UI compared to legacy bank dashboards

- Free for the core checking features

- Treasury and credit features grow with the business

Room for improvement

- US-only and tied to partner banks

- Underwriting is selective on the credit card

- Customer support is mostly async

Frequently Asked Questions

Is Mercury actually a bank?

Does Mercury cost anything?

Can non-US founders open a Mercury account?

Mercury vs Brex vs Ramp, which should I pick?

Does Mercury have an API?

Best For

Featured in

Alternatives to Mercury

View all

Reviews (3)

Mercury, better than expected

Got Mercury on the recommendation of someone I trust. What stands out is how modern UI compared to legacy bank dashboards. Treasury yields on idle cash works the way you'd hope. Found it works best for early-stage US startups opening their first bank account.

Pros

- Free for the core checking features

- Modern UI compared to legacy bank dashboards

- Treasury and credit features grow with the business

Finally something that fits

First impression of Mercury was 'huh, this is actually thought through.' Real selling point: treasury and credit features grow with the business. Main use case: founders consolidating banking, cards, and bill pay. Sticking with Mercury.

Pros

- Treasury and credit features grow with the business

Genuinely impressed

The pitch for Mercury sounded too good to be true. Mostly true. Genuine strength: free for the core checking features.

Pros

- Free for the core checking features

Badge builder

Add Mercury to your website

Choose a badge style and size, preview it here, then copy the generated HTML. Badge images are self-contained SVGs and do not require an external script.

<a href="https://toolindex.net/tools/mercury?ref=badge" target="_blank" rel="noopener">

<img src="https://toolindex.net/badge/mercury/medium.svg" alt="Mercury - Listed on Tool Index" width="180" height="50" />

</a>How to use the badge

- 1. Pick the style, size, and theme that fit your layout.

- 2. Copy the generated HTML from the code block.

- 3. Paste it into your footer, homepage, or press page.

Standard badge available

The standard listing badge is available now. Score and circle badges are limited to tools currently ranked in the top 10 of a category.

Badge clicks return visitors to this profile with a referral tag so the source remains identifiable.

Related Tools

Simple RMD

Calculate, aggregate, and manage your annual IRA required minimum distributions.

FreshBooks

Cloud accounting designed for service-based small businesses and freelancers

Deel

Global payroll, contractor, and EOR platform

Xero

Cloud accounting software for small businesses and their advisors