Nino

A dedicated CPA and CFP team plus AI to run your whole financial life for a flat fee

Gallery

About Nino

Nino is a personal financial planning service that pairs a dedicated team of credentialed professionals with AI-assisted planning software. Rather than handing you another dashboard and wishing you luck, it gives you a real CPA and a real CFP who build and maintain a single financial plan that stays current as your life changes. The pitch is that the kind of coordinated wealth management usually reserved for very affluent clients should be within reach of more people, at a flat fee.

The problem it's solving is fragmentation. Most people with a bit of financial complexity end up with their taxes in one place, their investments in another, their equity compensation in a spreadsheet, and their big decisions made in isolation. Nino's whole premise is to pull taxes, investments, stock options, cash flow, and real estate into one always-current plan, so those pieces actually talk to each other instead of being optimized separately and quietly pulling in different directions.

How it works is straightforward. You start with a short demo call, around 25 minutes, where the team looks for savings opportunities in your situation. From there an accountant and a planner build a personalized strategy, and then you meet for quarterly reviews to adjust as things change, whether that's a new job, a house, or a liquidity event. Because it's a managed service, the work happens on your behalf rather than being one more thing you have to drive yourself.

The scope of what the team handles is wide. There's tax optimization and filing, equity compensation and stock-option planning, retirement forecasting built on Monte Carlo simulations, modeling for a home purchase or other major life decisions, real estate planning, and estate and legacy work. Multi-state tax guidance is included for people whose lives cross state lines, and crypto holdings can be folded in through a CoinTracker integration so nothing important sits outside the plan. It's a lot for one person to hold in their head, and the point of bundling a CPA with a CFP is that the tax side and the planning side are handled by people who talk to each other rather than two separate professionals you'd otherwise have to coordinate yourself.

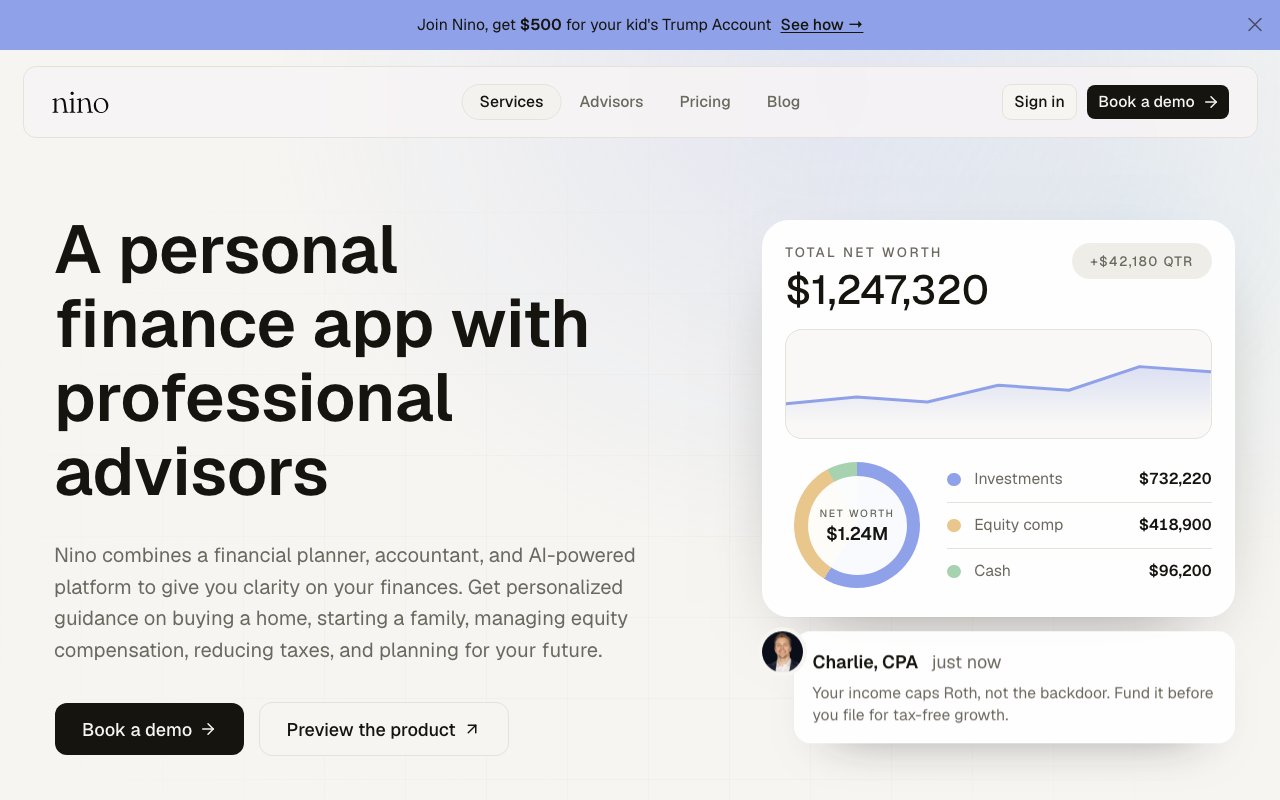

Underneath the advice, Nino aggregates your accounts so the team is always working from a full, current picture rather than whatever you happened to mention on a call. That's what lets the plan stay coordinated, since a decision about equity or a home purchase can be weighed against your taxes and cash flow at the same time instead of in a vacuum. The software handles the always-on modeling and monitoring while the humans make the judgment calls, which is the split the whole product is built around.

On the trust and security side, Nino connects to your accounts read-only and never moves your money, so it advises and plans without ever touching your funds. It uses bank-level encryption and states plainly that your data is never used to train AI. For anyone nervous about mixing an AI-forward product with their entire financial life, those boundaries are the reassurance that the humans and the software stay firmly in an advisory lane.

It's aimed at a specific kind of person. Founders, executives, and professionals with stock options, multiple accounts, or business income are the sweet spot, along with higher-net-worth families who need coordinated tax and financial planning. If your finances are a single paycheck and a savings account, this is more than you need. If you've got equity, several income sources, and decisions that interact in complicated ways, that's exactly the mess it's built to untangle. The flat fee tends to look most reasonable for exactly this group, since a percentage-based advisor gets more expensive as your assets grow while Nino's price stays put no matter how large the plan it's managing becomes.

Pricing is a flat annual fee rather than a percentage of your assets, which is a meaningful break from traditional advisors who take a slice of everything you own. The tiers run from Core at $2,000 a year, to Plus at $3,500, to Ultra at $6,000 and up, with tax filing available as an add-on that costs extra at each level. There's a 30-day money-back guarantee and you can cancel anytime, so the commitment is lower than the annual figure suggests. Access starts with a demo call rather than instant signup, since the service depends on matching you with a team, and that call doubles as a chance to see whether the savings it finds would cover the fee before you commit to anything.

Key Features

- Dedicated CPA and CFP advisory team

- AI-assisted always-current financial plan

- Tax optimization and filing

- Equity compensation and stock-option planning

- Retirement forecasting with Monte Carlo simulations

- Read-only account aggregation

Pros & Cons

What we like

- Pairs real human CPAs and planners with software

- Flat annual fee instead of a percentage of assets

- Coordinates tax, investing, and equity in one plan

- Read-only connections, so it never moves your money

Room for improvement

- Expensive, starting at $2,000 a year

- No free tier or self-serve option

- Tax filing costs extra on top of the plan

- Aimed at higher earners, not simple finances

Frequently Asked Questions

What is Nino?

How much does Nino cost?

Does Nino manage or move my money?

Who is Nino for?

Best For

Featured in

Alternatives to Nino

View all

Reviews (10)

Recommended without reservation

Nino solves a real problem for me without making a fuss about it. Got real value out of tax optimization and filing. The output quality holds up better than I expected. Easy yes for anyone weighing the same trade offs.

Worth a look

Nino solves a real problem for me without making a fuss about it. The thing I keep coming back to is how reliable it is. Mostly using it for modeling retirement with monte carlo forecasts. It earns its place in my stack.

Two months in, no regrets

Came to Nino after getting frustrated with what I had before. The retirement forecasting with monte carlo simulations is more useful than I expected. The thing I keep coming back to is how reliable it is. Would sign up again without thinking twice.

It just works

Picked Nino for the price, stayed for the quality. It does what it says, which is rarer than it should be. Hard to imagine going back to my old setup.

Worth a look

Nino has quietly become part of my daily flow. It does what it says, which is rarer than it should be. It fits well for planning a home purchase across multiple accounts. Worth it for what I get out of it.

Solid but not perfect

Came to Nino after getting frustrated with what I had before. Got real value out of read-only account aggregation. Found it works best for coordinating tax and investing around startup equity. It would be a five if not for expensive, starting at 2,000 a year. Hard to imagine going back to my old setup.

Finally something that fits

Hadn't planned on switching, but Nino was hard to ignore. Got real value out of flat annual fee instead of a percentage of assets. It fits well for planning a home purchase across multiple accounts.

Quietly excellent

Nino solves a real problem for me without making a fuss about it. It handles the boring parts so I can focus on the work that matters. The defaults are sensible, so I was not fighting settings on day one. Easy yes for anyone weighing the same trade offs.

Decent with some rough edges

Three months of Nino later, here is what holds up. Where it really wins is equity compensation and stock-option planning. It would be a five if not for no free tier or self-serve option. Hard to imagine going back to my old setup.

Quietly excellent

Have been running Nino for a while, here is where I land. Their take on ai-assisted always-current financial plan is genuinely good. Found it works best for coordinating tax and investing around startup equity. Recommending it to people in a similar spot.